Your everyday UPI payments could be earning you nothing, and costing you lakhs over time. Discover how switching from debit to a rewards-driven card like LevelUP can turn your monthly spends into real savings and long-term value.

India crossed 16,000 crore UPI transactions last year. If you're reading this, you were probably responsible for a few thousand of them, groceries, Swiggy orders, auto rides, bill payments, the occasional splurge.

Here's the uncomfortable question: how much did you earn from any of it?

If you paid using a debit card linked to PhonePe, Google Pay, or Paytm, the answer is zero. Not "almost nothing." Literally ₹0. Every scan, every transfer, every QR code tap: ₹0 back in your pocket.

We ran the actual numbers. Not in percentages, in rupees. And the total, once you see it laid out across a career, is genuinely difficult to look at.

First, let's be precise about what "₹0" means

There's a version of this conversation that floats around fintech Twitter: "Indians leave money on the table by not using rewards cards." True but vague. We want to be specific.

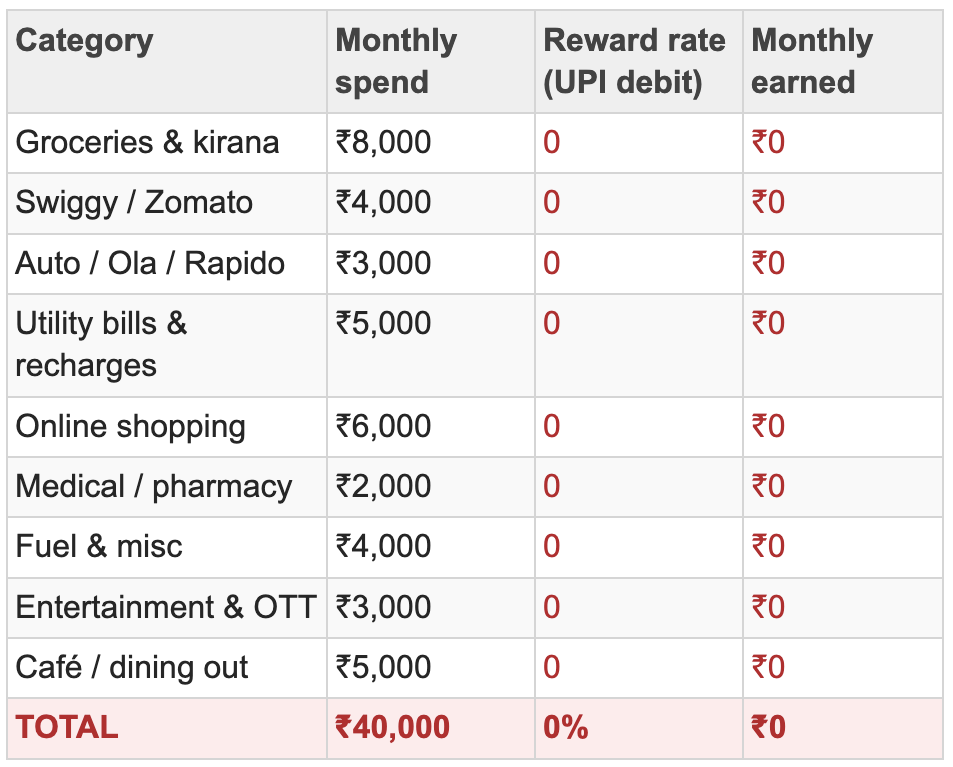

The average Indian salaried professional in a metro spends approximately ₹40,000 per month on UPI. That number comes from RBI data on per-card average transaction values and Redseer's research on digital payment categories. Let's map it out:

How ₹40,000/month breaks down, and what debit UPI earns on each

Nine categories. ₹40,000 in monthly spending. ₹0 earned. Every month.

Now let's calculate what that actually costs you over time.

The opportunity cost, year by year

We benchmarked against a conservative 5% reward rate, the floor on what a well-designed RuPay credit card on UPI can return. Here's what the gap looks like across a career:

What you're giving up, ₹40,000/month UPI spend, debit vs. 5% reward card

Over 5 years of your career, the cost of using a debit card for UPI isn't inconvenience. It's ₹1,20,000 in rewards that evaporated into the air.

That's not a rounding error. That's a Solo Europe trip. A laptop. Four months of EMI on a used car. Money that was functionally yours, you spent it, you generated the transaction, but the bank kept the value and gave you nothing.

Now let's do the LevelUP math

The SalarySe LevelUP card isn't a generic "get 1% back" offer. Its reward structure is tiered and specifically designed around how a salaried professional actually spends: heavier toward month-end, with a spike on payday. Here's what the same ₹40,000 monthly spend earns on LevelUP:

What the same ₹40,000/month earns on LevelUP

₹2,275 to ₹4,475 every single month. Not once. Not as a sign-up bonus. Every month, on spending you were going to do anyway, on the same Swiggy order, the same kirana bill, the same auto ride.

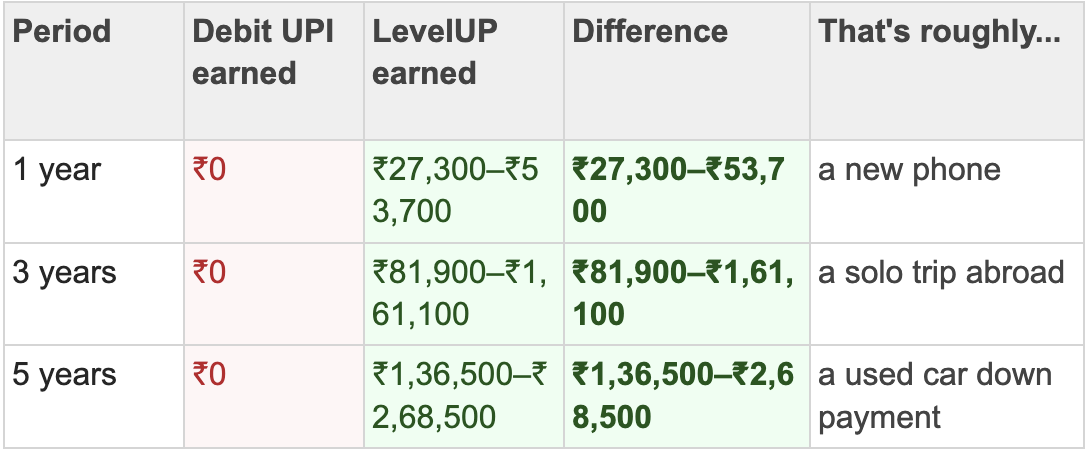

The full career comparison

Now stack that up against doing nothing, against staying on debit UPI the way most people do:

Debit UPI vs. LevelUP - 5-year career comparison

Five years of salaried life. Same spending. The only variable: whether your UPI payments earn anything or not.

"But I already have a credit card"

Fair. And if you're paying your full statement balance every month and earning rewards on UPI, you're already ahead of most people. This section isn't for you.

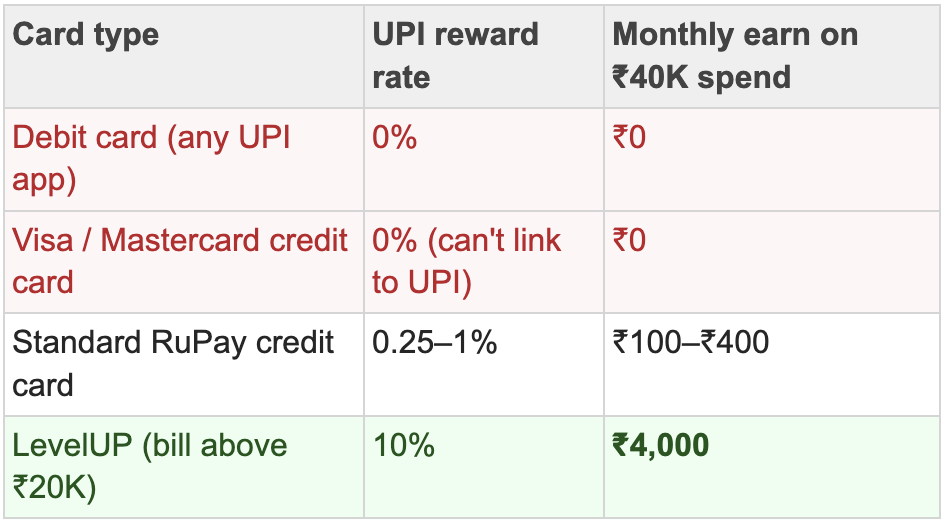

But here's the reality check most people miss: the majority of credit cards in India ,HDFC, ICICI, Axis, SBI, are Visa or Mastercard. They physically cannot link to UPI. So if you're using Google Pay or PhonePe to pay, you're paying from your bank account, not your credit card. The rewards on that spend? Zero.

Even if you have a RuPay credit card linked to UPI, check what you're actually earning. Most standard RuPay cards give 0.25% to 1% on UPI transactions. On ₹40,000 of monthly spend, that's ₹100 to ₹400 a month, better than nothing, but a fraction of what a well-structured card returns.

The honest version of this comparison looks like this:

UPI reward rates, what most cards actually pay

No card is perfect. LevelUP's 10% accelerated rate applies when your monthly bill crosses ₹20,000, so if you're a lighter spender, you're in the 5% tier. The 37.5% Salary Day Bonus is real but capped: it applies only on the 1st and last day of the month via SalarySe UPI, with a maximum of 5,625 reward points per month. On a typical month, most users will land somewhere between ₹2,000 and ₹3,500 in monthly rewards, not the ceiling, but meaningfully more than any alternative in this category.

The real question isn't "should I switch"

It's simpler than that. Every month you spend ₹40,000 on UPI without a reward card, that money is gone. You can't reclaim it. You can't retroactively earn on last month's Swiggy orders or last year's grocery runs.

The 16,000 crore transactions that happened in India last year earned ₹0 in rewards for the vast majority of people who made them. That's not a statistic about India. That's a statistic about you, me, and every salaried professional using a debit UPI app as their default payment method.

The switch costs nothing, literally ₹0 on the virtual LevelUP card. The opportunity cost of not switching is now something you can calculate exactly.

One year: ₹27,300 to ₹53,700. Three years: ₹81,900 to ₹1,61,100. Five years: ₹1,36,500 to ₹2,68,500. All of it from the spending you were already planning to do.

That number is sitting on the table. The only question is who picks it up.

SalarySe raises $11.3M to redefine credit access for India’s workforce. Led by Flourish Ventures and SIG Venture Capital, with support from Peak XV Partners and Pravega Ventures, the funding will fuel AI-led innovation, enterprise expansion, and smarter financial solutions for salaried professionals.

What organisations are calling quiet quitting is often financial anxiety presenting as disengagement. Smart employers are addressing the root cause, not the symptom.

India's employee Benefits landscape is shifting from slow, manual reimbursements to intelligent, real-time tax savings, and forward-thinking HR leaders are already making the switch.