India's real economy runs on small payments, chai, autos, kiranas, Swiggy orders. Here's why these micro-transactions under ₹500 are now the most valuable swipes you make, and how to actually earn from them.

.png)

There is a transaction happening right now, somewhere in India, that no bank executive would have cared about five years ago.

Someone is paying ₹20 for a cutting chai by scanning a QR code.

Or ₹60 to an auto driver on the way to work.

Or ₹340 at the kirana store around the corner for milk, bread, and a packet of biscuits.

Individually, these feel like rounding errors in a monthly budget. Collectively, they are the backbone of one of the largest payment economies on the planet. India processed over 16,000 crore UPI transactions in 2024–25. The overwhelming majority of them were small. Unremarkable. Routine.

And for most Indians making these payments, every single one of them earned absolutely nothing.

That is about to change, if you have the right card.

India has always been a micro-transaction economy. The street vendor, the neighbourhood grocery shop, the auto driver, the local dhaba, these are not edge cases in the Indian spending story. They are the centre of it.

For decades, these transactions were cash-only by default. Then UPI arrived and quietly digitised them. The chai wala got a QR code printed on a laminated sheet. The kirana uncle started accepting Google Pay. The auto driver who never had a card machine in his life now has a PhonePe sticker on his windshield.

Today, a transaction as small as ₹5 can happen digitally in India. And it frequently does.

What this created, without most people realising it, is an enormous pool of daily spending that is trackable, digital, and in theory, rewardable. The problem is that almost no credit card in India was designed to reward it.

Pick up any premium credit card in India and read the fine print. You will find the same pattern every time.

5% cashback on Swiggy minimum order ₹300, capped at ₹150 per month. 10% on Amazon, only on weekends, only above ₹1,000. Lounge access, unlock it by spending ₹20,000 last month. Fuel surcharge waiver, only between ₹400 and ₹4,000 per transaction.

Every benefit has a floor. Every reward has a threshold. Every perk assumes you are spending in large, deliberate chunks, not in the scattered, daily, ₹40-here-₹200-there pattern of how most Indians actually live.

This is not an accident. Traditional credit cards were designed for a different era of spending. EMIs on electronics, restaurant bills, hotel bookings, flight tickets. The ₹500 transaction was beneath their architecture.

And then RuPay changed everything.

When the National Payments Corporation of India enabled RuPay credit cards to be linked to UPI, it did something structurally significant that most people still haven't fully processed.

It made credit card rewards possible at the point where India actually spends money.

Not at the mall. Not on a travel booking website. At the QR code. At the kirana. At the chai stall. At the auto stand.

For the first time, a credit card could sit inside the same payment flow as the ₹40 chai. The same tap-and-pay moment that was previously reserved for debit cards and bank accounts, earning nothing, could now earn reward points, generate cashback, and contribute to monthly spend thresholds.

This is the structural shift that most Indians have not caught up with yet. The instrument changed. The behaviour, scanning a QR code, stayed exactly the same. But the financial outcome became completely different.

The person paying ₹40 for chai with a debit card and the person paying ₹40 for chai with a RuPay credit card linked to UPI are doing the same physical action. One of them is leaving money on the table. Every single day.

Here is where it gets interesting. Because while ₹40 sounds trivial, the actual monthly volume of micro-spending for a typical urban salaried Indian is anything but.

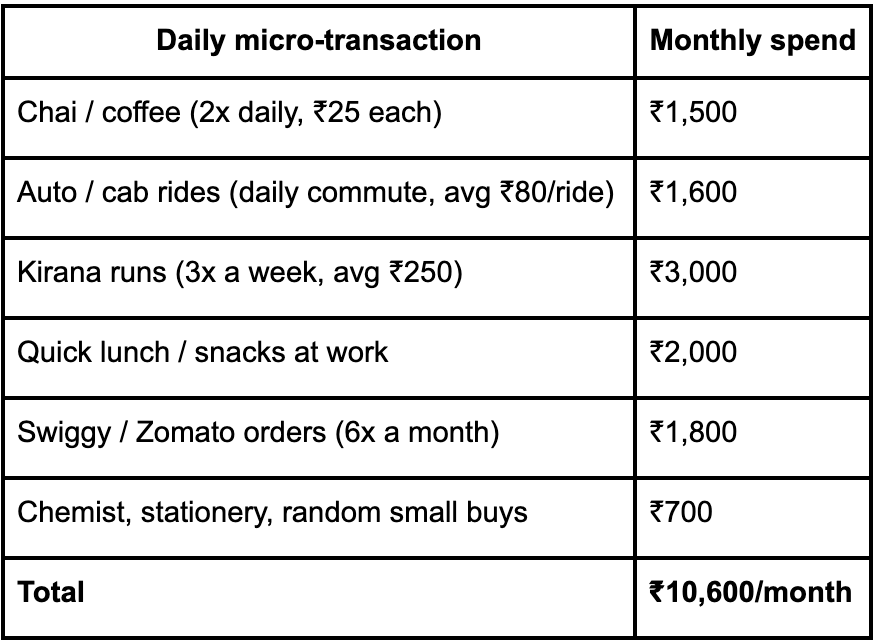

Think about a regular month:

₹10,600 in micro-transactions every month. That is not a small number. That is a significant chunk of a salaried Indian's take-home pay, spent in transactions that are individually forgettable but collectively enormous.

Now run that through the SalarySe LevelUP card's reward structure on SalarySe UPI.

If your total monthly spend crosses ₹20,000 and you unlock Super Accelerated Rewards at 10 RP per ₹100, that same ₹10,600 in micro-spending generates 1,060 Reward Points, worth ₹212.

And this is before the Salary Day Bonus enters the picture. On the 1st and last day of every month, every transaction via SalarySe UPI earns 25 Reward Points per ₹100. Time your bigger kirana shop or monthly subscription payments on those two days and the rewards from a single grocery run jump significantly.

₹1,500 kirana run on the 1st of the month → 375 Reward Points → ₹75 back. From one grocery trip.

None of this required you to spend differently. You shopped where you always shop. You paid how you always pay, by scanning a QR code. You just swapped the instrument.

This is the part that still surprises most people.

You do not need a specific merchant to be "partnered" with LevelUP to earn rewards. You do not need to shop at a curated list of brands or download a separate offers app. Any merchant in India with a UPI QR code, and that is now tens of millions of them, from organised retail all the way down to the vegetable cart outside your building, becomes a rewards opportunity the moment you pay via SalarySe UPI.

The chai wala's QR code. The kirana uncle's PhonePe sticker. The auto driver's payment link. The neighbourhood salon that started taking UPI during the pandemic and never went back to cash. All of them. Every scan earns.

This is what makes the RuPay-UPI combination genuinely democratising. Premium credit card rewards have historically been concentrated in organised retail, branded stores, airlines, hotel chains, large e-commerce platforms. The informal economy that most Indians actually live in was invisible to the rewards system.

Not anymore. The ₹20 chai is now as rewardable as the ₹2,000 flight booking. The system finally caught up with the way India actually spends.

There is a deeper story underneath the maths.

India's middle class built its relationship with money around the principle of careful spending, ek ek paisa ka hisaab. The kirana run was budgeted. The chai was counted. The auto ride was a necessary expense, not a rewarding one.

Credit cards entered this picture with a reputation for encouraging overspending, for trapping people in interest cycles, for being tools of the financially reckless. That reputation was not entirely undeserved, in an era when credit cards required large spends to justify their fees and rewarded behaviour that most ordinary Indians simply did not engage in.

RuPay credit cards linked to UPI flip this entirely. A card like LevelUP does not ask you to spend more. It does not ask you to change your habits, upgrade your lifestyle, or hit aspirational thresholds. It asks you to keep doing exactly what you are already doing, paying for chai, groceries, autos, lunch, and simply use a different payment instrument.

This is credit that works with the grain of Indian spending behaviour, not against it. The ₹500 transaction is no longer beneath the system. It is at the centre of it.

The careful spender who has always done ek ek paisa ka hisaab is now, paradoxically, the person who benefits most from this system. Because their spending is already disciplined. They pay their bill in full every month. They do not revolve credit. They just want something back for money they were always going to spend. LevelUP is built for exactly that person.

The practical shift is simpler than most people expect.

You do not need to change where you shop. Your kirana uncle's QR code works with SalarySe UPI just as it works with Google Pay or PhonePe. The chai wala's sticker accepts RuPay credit card payments through UPI. The auto driver's payment link works the same way.

What changes is the instrument you use when you scan. Instead of hitting your savings account every time, you hit your LevelUP credit card, earning reward points, building your credit score, and keeping your salary in your account for longer.

The points accumulate quietly across every transaction, the ₹40 chai, the ₹80 auto, the ₹340 kirana run, until you have enough to redeem it on the SalarySe app. No complex redemption portal. No category restrictions on how you spend the value back. Just real money, returned to you from the spending you were always going to do.

Over a year, ₹10,600 a month in micro-transactions at the accelerated 5 RP rate adds up to ₹1,272 back annually, just from small, everyday spending. Cross the ₹20,000 monthly threshold and unlock Super Accelerated Rewards, and that same micro-spending returns ₹2,544 a year.

From chai. From autos. From the kirana around the corner.

India's real economy has always run on small transactions. What changed is that those transactions are now digital, trackable, and, for the first time, genuinely rewardable.

The gap between someone who earns from these transactions and someone who doesn't is not income. It is not spending power. It is simply the card in their phone's UPI app.

The chai is ₹40. The auto is ₹80. The kirana run is ₹340.

Together they are probably ₹10,000 of your month. Individually, they feel like nothing. Collectively, with the right card, they are a meaningful amount of money coming back to you every single year, for doing absolutely nothing differently.

SalarySe raises $11.3M to redefine credit access for India’s workforce. Led by Flourish Ventures and SIG Venture Capital, with support from Peak XV Partners and Pravega Ventures, the funding will fuel AI-led innovation, enterprise expansion, and smarter financial solutions for salaried professionals.

What organisations are calling quiet quitting is often financial anxiety presenting as disengagement. Smart employers are addressing the root cause, not the symptom.

India's employee Benefits landscape is shifting from slow, manual reimbursements to intelligent, real-time tax savings, and forward-thinking HR leaders are already making the switch.