Avoid the credit card “minimum due” trap that keeps you stuck in high-interest debt. Learn how it works, why it’s costly, and how smarter choices like paying in full or using salary-aligned cards like LevelUP can protect your finances.

You receive your credit card bill. It's ₹30,000. Life is tight this month, rent just went out, you have EMIs, the usual. So you spot that small line at the bottom: Minimum Amount Due: ₹1,500.

You pay the ₹1,500. You feel responsible. You avoided a late fee. No red mark on your credit score. Job done.

Except, you just stepped into one of the most elegantly designed financial traps in the banking industry. And every month you stay in it, the walls close a little tighter.

Here's exactly what's happening to your money.

What the minimum due actually means

Banks in India are required by RBI to set a minimum due, typically 5% of the outstanding balance, or ₹200, whichever is higher. On the surface this sounds like a helpful safety net. In reality, it's designed to do one thing: keep you in debt for as long as possible.

When you pay only the minimum due, your bank does not treat the remaining balance as settled. It treats it as a revolving balance, and starts charging interest on the entire original bill, not just the unpaid portion. That interest rate? Between 36% and 48% per annum for most Indian credit cards.

"You don't pay interest on what you didn't pay. You pay interest on everything, from the day of each purchase."

That distinction matters enormously. Let's run the real numbers.

The math that banks don't show you

Meet Arjun. He's a 26-year-old software engineer in Bengaluru earning ₹65,000/month. He spent ₹30,000 on his credit card this month. Groceries, Zomato orders, a weekend trip, some online shopping. He pays the minimum due of ₹1,500 and decides he'll clear the rest next month.

Arjun's situation

Here's what happens over the next 6 months if Arjun keeps paying just the minimum, and stops adding new charges to the card.

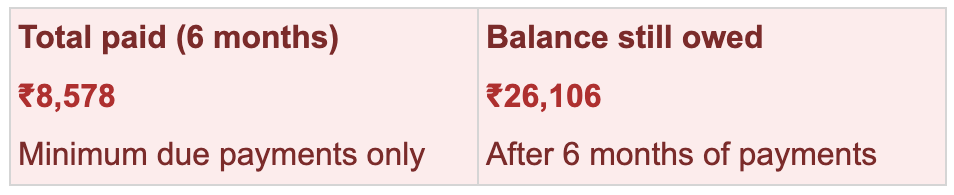

After 6 months and ₹8,578 paid, Arjun still owes ₹26,106, barely ₹2,400 less than what he started with. He's essentially been renting the debt. Of every rupee he paid, more than 73% went straight to interest.

At this rate, paying only the minimum, no new spends, it would take Arjun over 5 years to clear a single month's ₹30,000 bill. Total interest paid: north of ₹22,000. On a bill he originally spent on groceries and weekend plans.

The hidden mechanic: no interest-free period once you revolve

Here's the part that catches even financially aware people off-guard. Once you start revolving, i.e., carry a balance, you lose your interest-free grace period entirely on all new purchases too.

So if Arjun buys something for ₹2,000 the month after, that ₹2,000 starts attracting interest from day one, not after the statement date. The grace period, which most credit cards advertise as 45–50 days, disappears the moment you don't pay in full.

This is the compound trap: old debt is growing, new purchases are immediately expensive, and the minimum due feels manageable enough to not alarm you.

Why the minimum is designed this way

The minimum due is not consumer protection, it's a revenue mechanism. Banks make enormous margins on revolving credit. RBI data shows that credit card interest and fee income is one of the highest-yield products a bank carries. The minimum due is calibrated to keep the customer current (no default, no bad debt on the bank's books) while maximising the interest-earning balance. Everyone wins, except the person paying it.

"The minimum due is low enough to feel affordable, high enough to avoid a default, and perfectly sized to keep you in debt for years."

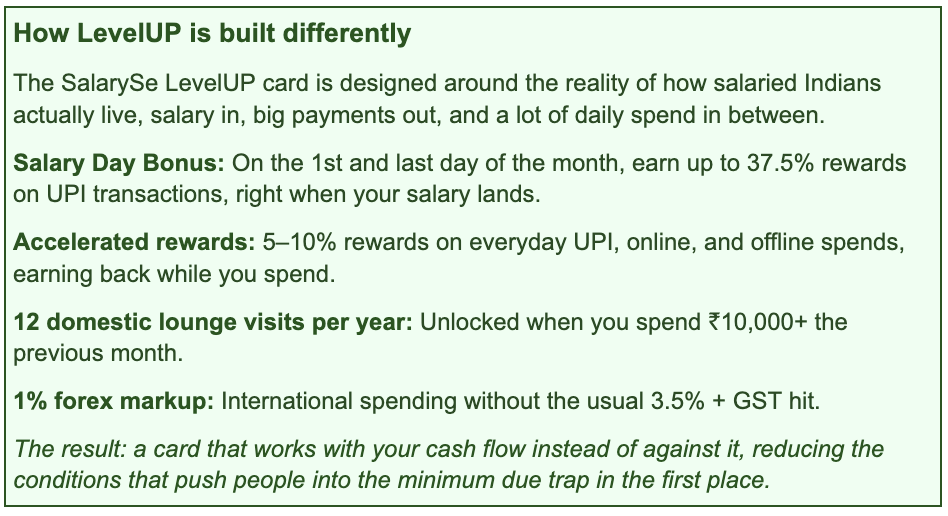

How LevelUP is built differently

Most credit cards are indifferent to when your salary arrives relative to your bill. You spend through the month, the statement generates, and you're expected to pay, whether or not you've been paid yet. If your salary comes on the 5th and your bill is due on the 2nd, the timing alone can force you into the revolving trap.

The SalarySe LevelUP card is designed around the reality of how salaried Indians actually live: salary in, big payments out, and a lot of daily spend in between.

The rule that actually saves you

There's one principle that cuts through everything: never spend on a credit card what you cannot pay in full on the due date. It sounds obvious. It almost never gets followed. Because the minimum due makes overspending feel survivable, until it isn't.

If you do find yourself with a balance you can't clear, here's what to do:

Pay more than the minimum, always. Even paying 20–25% of the outstanding balance instead of 5% dramatically reduces the total interest you pay and the time you spend in debt.

Stop spending on that card until it's cleared. New purchases on a revolving card are immediately expensive.

Set up an autopay for the full statement balance if your salary timing allows. This ensures you never accidentally revolve due to forgetting to pay.

Pick a card whose billing aligns with your payday. This is the structural fix, and it's why the LevelUP card's salary-linked design matters more than any individual reward rate.

The minimum due isn't a lifeline. It's a slow leak in your financial floor. The month you choose to pay in full, or the card you choose that makes that easier, is the month the trap stops working.

SalarySe raises $11.3M to redefine credit access for India’s workforce. Led by Flourish Ventures and SIG Venture Capital, with support from Peak XV Partners and Pravega Ventures, the funding will fuel AI-led innovation, enterprise expansion, and smarter financial solutions for salaried professionals.

What organisations are calling quiet quitting is often financial anxiety presenting as disengagement. Smart employers are addressing the root cause, not the symptom.

India's employee Benefits landscape is shifting from slow, manual reimbursements to intelligent, real-time tax savings, and forward-thinking HR leaders are already making the switch.