This blog uses sneaker culture as a hook to explain key investing lessons—supply & demand, asset appreciation, compounding, diversification, and liquidity—while offering practical strategies for salaried professionals to build smarter, long-term financial portfolios.

Nike announces a new pair of Jordans. Supply is capped at 5,000 pairs. Within minutes, the sneakers are gone, reselling at five times the price on StockX. What just happened?

Behind the flashy sneaker world lies the same principles that run the stock market. And if you look closely, you’ll see why sneaker culture is one of the best metaphors for investing.

Why does a ₹15,000 sneaker resell at ₹70,000? Simple: limited supply, soaring demand. The same rule drives asset prices.

SalarySe Says: Before investing in any asset, ask: what drives its demand, and how scarce is its supply? A company with unique products and limited competition has the same advantage as Nike dropping a rare pair - its value is likely to rise.

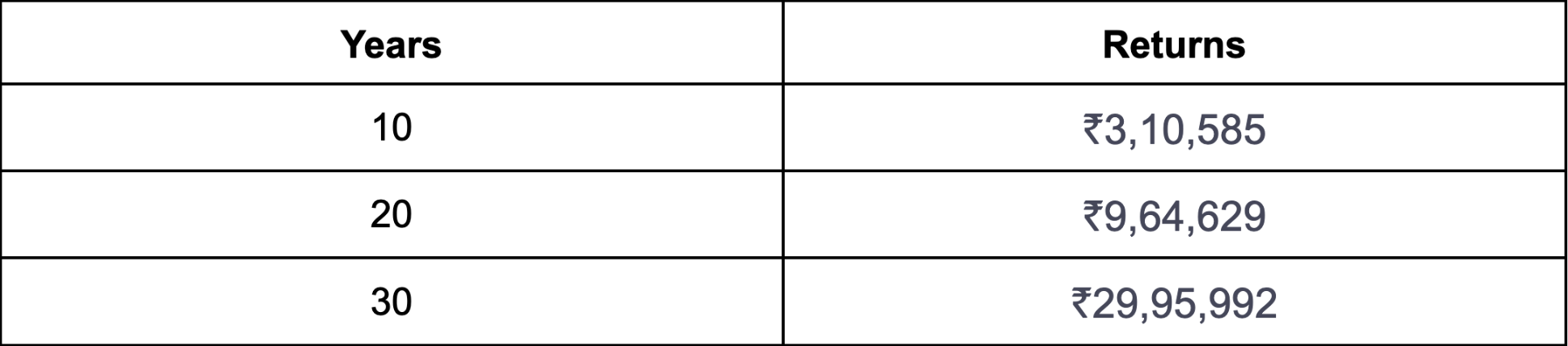

Sneakers bought at retail appreciate if they become desirable over time. The earlier you buy, the higher your return. Investing works the same way.

Same SIP, but the early starter ends up with 3.5x more wealth, just like sneakerheads who buy early and hold.

SalarySe Says: Time matters more than timing. Start early, even small amounts multiply with compounding.

Sneakerheads know “deadstock” (unworn pairs) fetches the highest resale value. The longer you hold, the rarer they get. Similarly, investors who hold through volatility enjoy the compounding effect.

SalarySe Says: Wealth isn’t built in the first 5 years—it’s in the next 20. Selling early cuts off compounding just when it’s getting powerful.

Sneakerheads rarely buy just one brand. They spread bets—Nike, Yeezy, Puma collabs. Some appreciate, some don’t. Investors must do the same.

Balanced Portfolio Example (for a ₹50,000/month earner):

SalarySe Says: Diversification isn’t just about risk—it ensures consistent growth across good and bad market cycles.

Sneaker resale value is only real if you find a buyer. Same with investments that liquidity matters.

SalarySe Says: Always align investments with your goals. Short-term goals → liquid assets. Long-term goals → growth assets.

Sneakers are culture; investing is wealth-building. The overlap lies in principles: supply-demand, scarcity, patience, and strategy. But while sneakers are speculative and taste-driven, investing can be structured, diversified, and goal-oriented.

SalarySe Says: For salaried professionals, blending assets is key. A SalarySe RuPay Credit Card helps you earn cashback on everyday UPI spends (free money back on what you already do). Combine that with SIPs (growth) and FDs (stability), and you’ve built a diversified “sneaker wall” of financial assets.

In the sneaker world, the rarest pairs fetch the highest bids. In the investing world, the rarest trait - patience - fetches the highest wealth.

So, the next time you see a sneakerhead flex his collection, remember: your financial portfolio can be just as flex-worthy, if you play the long game.

SalarySe raises $11.3M to redefine credit access for India’s workforce. Led by Flourish Ventures and SIG Venture Capital, with support from Peak XV Partners and Pravega Ventures, the funding will fuel AI-led innovation, enterprise expansion, and smarter financial solutions for salaried professionals.

What organisations are calling quiet quitting is often financial anxiety presenting as disengagement. Smart employers are addressing the root cause, not the symptom.

India's employee Benefits landscape is shifting from slow, manual reimbursements to intelligent, real-time tax savings, and forward-thinking HR leaders are already making the switch.